What Happens If the IRS Audits Your Small Business?

An IRS audit of your small business is one of the most feared phone calls in business ownership — and one of the least understood. Most small business owners have never seen the actual letter, don’t know what triggers one, and have no idea what the process actually involves.

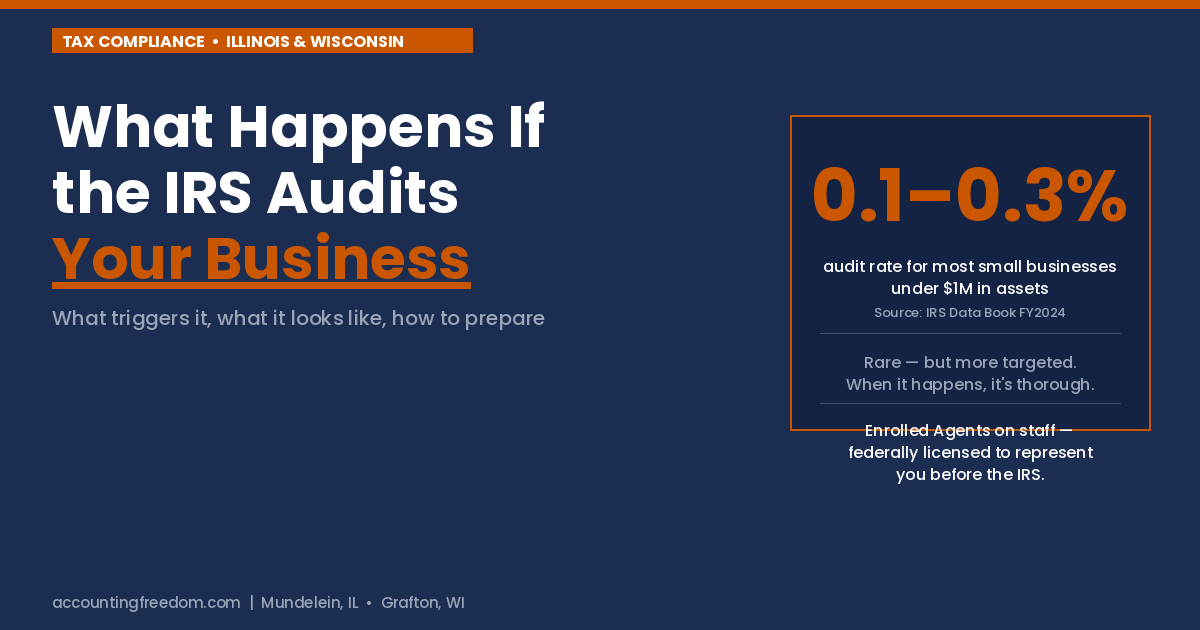

Here’s the good news first: an IRS audit of a small business is genuinely rare. The bad news: when it happens, not knowing what to expect makes a manageable process feel like a crisis. This post covers what actually triggers an IRS audit, what the process looks like step by step, and what Illinois and Wisconsin small business owners should do if that letter arrives.

The short version: Small business IRS audit rates are low — the FY2024 IRS Data Book shows audit rates for most small businesses under $1M in assets running between 0.1% and 0.3%. But the audits that do happen are more thorough than ever, as the IRS relies increasingly on AI and automated data matching to select returns. The most common triggers are income that doesn’t match third-party reporting, deductions that look disproportionate to your revenue, repeated business losses, and worker misclassification. Most audits are handled entirely by mail. The best defense is clean documentation and a professional who can represent you — which is exactly what an Enrolled Agent does.

How Likely Is an IRS Audit for Your Small Business?

Audit rates for small businesses are genuinely low. The FY2024 IRS Data Book shows the IRS examined C-corporations with assets under $1M at a 0.1%–0.2% rate. S-corporations and partnerships saw rates too low to be statistically significant. For context: the IRS closed just over 505,000 total audits in FY2024 across all return types — out of more than 266 million returns processed.

That said, there’s an important caveat. Lower audit rates don’t mean less enforcement. The IRS closed FY2024 with $29 billion in recommended additional taxes from those audits, and collected nearly $77.6 billion through its collection function — up 13.6% from the prior year. The agency is doing more with less: fewer audits, but more targeted ones, backed by AI and automated data-matching that can flag discrepancies across 4.6 billion information returns simultaneously.

What Actually Triggers an IRS Audit

The IRS uses an automated scoring system called the Discriminant Income Function (DIF) to rank every return by how much it deviates from statistical norms for similar businesses in the same industry and revenue range. A high DIF score doesn’t guarantee an audit, but it significantly increases the odds of one. Here are the patterns that drive that score up.

Income That Doesn’t Match Third-Party Reporting

The IRS cross-references your reported income against 1099s, W-2s, bank records, and payment processor data from platforms like Stripe, Square, PayPal, and Venmo. Any mismatch is essentially automatic. This is the single most common audit trigger — and it’s also the easiest to avoid, since it requires no judgment call, just accurate reconciliation.

Deductions That Look Disproportionate to Your Revenue

The IRS compares your deduction ratios against industry norms for businesses your size. A landscaping company deducting unusually high travel expenses, or a restaurant claiming an outsized home office deduction, raises a flag — not because the deduction is necessarily improper, but because it deviates from what’s typical for that type of business.

Round numbers compound this risk. A return with several deductions ending in 0 or 5 — $6,000 for advertising, $4,000 for vehicle expenses — signals estimation rather than recordkeeping, which draws additional scrutiny.

Repeated Business Losses

A business that reports losses in three or more of the last five years invites a specific question from the IRS: is this a legitimate profit-seeking business, or a hobby being used to generate tax write-offs? Legitimate businesses absolutely can run multi-year losses — but the documentation supporting that needs to be solid if the pattern continues.

Worker Misclassification

Calling an employee a 1099 contractor to avoid payroll taxes is one of the more aggressively pursued audit areas, particularly for contractors, landscaping companies, and other businesses that rely on field labor. The IRS’s test centers on control: if you direct when, how, and where the work happens, that’s an employee — regardless of the label on the contract.

High Cash Transaction Volume

Cash-heavy businesses face elevated scrutiny because cash is harder to verify against third-party records. A specific pattern the IRS watches for: declining credit card revenue alongside stable overall reported income — a signal that can suggest cash income isn’t being fully reported.

What Actually Happens During an IRS Audit of a Small Business

Most small business owners picture an audit as IRS agents showing up at the door. In reality, the overwhelming majority of audits are handled entirely through the mail.

| Audit Type | How It Works | What to Expect |

|---|---|---|

| Correspondence Audit | Conducted entirely by mail | Most common type. IRS requests specific documentation to support an item on your return — usually resolved by sending the requested records. |

| Office Audit | In-person meeting at an IRS office | You (or your representative) bring requested records to a scheduled appointment to walk through specific return items. |

| Field Audit | IRS agent visits your business or representative’s office | The most thorough audit type. Reserved for more complex returns or larger discrepancies. Yields significantly more revenue recovery than the other two types — meaning these are typically more serious. |

Regardless of which type you’re facing, the process generally follows the same path:

- You receive a notice. This identifies the specific items under review and what documentation the IRS wants to see. It is not an accusation — it’s a request for substantiation.

- You gather and submit documentation. Receipts, bank statements, mileage logs, invoices — whatever supports the items in question. This is where clean, organized books make the difference between a quick resolution and a drawn-out process.

- The IRS reviews and responds. Either they accept your documentation as sufficient, propose adjustments to your tax liability, or request additional information.

- You resolve the audit. If you agree with the findings, you pay any additional tax owed. If you disagree, you have the right to appeal — and this is a point where professional representation matters most.

How Illinois and Wisconsin Small Business Owners Can Reduce Audit Risk

Most audit risk is preventable — not through aggressive tax avoidance, but through the same things that make for good bookkeeping in general.

Keep Income and Reporting in Sync

- Reconcile every income source against third-party reporting. Before filing, compare your reported income against every 1099, payment processor statement, and bank deposit. Income mismatches are the single most common trigger — and entirely within your control to prevent.

- Avoid round numbers. Returns with deductions ending in $0 or $5 signal estimation rather than recordkeeping. Use your actual figures every time.

Document Deductions Properly

- Go beyond the receipt. A receipt alone often doesn’t survive scrutiny. Vehicle logs, written business purpose notes, and meeting records are what hold up when a deduction gets questioned.

- Check your deduction ratios against industry norms. If your meals, vehicle, or home office deductions look unusually high relative to your revenue and your industry, review them before filing — not after a notice arrives.

Get Worker Classification and Payroll Right

- Resolve borderline worker classification proactively. If any worker’s status isn’t clear-cut, the IRS’s Form SS-8 lets you request an official determination before it becomes an audit issue.

- Keep payroll tax deposits current and on schedule. Late or inconsistent deposits are a direct, easily detected trigger — and one of the most avoidable.

- Use accounting software that maintains a clean audit trail. Cloud-based bookkeeping with consistent categorization gives you and your accountant a defensible record when questions arise.

None of this requires aggressive planning or unusual systems. It requires accurate, current bookkeeping — the kind that falls through the cracks when a business relies on a tax-only preparer who touches the books once a year in February.

Why Representation Matters If You’re Audited

If you receive an audit notice, who represents you matters — and not every tax preparer can represent you before the IRS.

Enrolled Agents hold a federal license specifically to represent taxpayers before the IRS — in audits, appeals, and collections matters. Unlike a basic seasonal preparer, an Enrolled Agent can communicate directly with the IRS on your behalf, attend meetings in your place, and negotiate resolutions. At Accounting Freedom, our Client Advisors include Enrolled Agents. That means representation isn’t a service we’d refer out — it’s built into the relationship.

What This Means for Your Business

An IRS audit is rare, and most small businesses survive one without drama — provided the books were clean to begin with and someone qualified is in their corner when the notice arrives.

The businesses that handle audits well aren’t the ones with nothing to hide. They’re the ones with organized records, accurate reconciliations, and a relationship with an advisor who already knows their business — rather than meeting their representative for the first time after the letter shows up.

- See what proactive monthly accounting looks like: Use our pricing calculator — no email required.

- Not sure which tier fits your business: Take our two-minute package assessment.

Already received an IRS notice — or want to make sure you never do?

A free consultation gets you a real look at your books and where the risk actually sits. Enrolled Agents on staff, ready to represent you if it’s ever needed.

Schedule a Free Consultation Contact UsDisclaimer: This article is provided for general informational purposes only and does not constitute tax, legal, accounting, or financial advice. Every business situation is different. Before acting on anything you read here, please consult with a qualified advisor — including, we hope, us. Reach out to Accounting Freedom for guidance specific to your situation.

About the Author

Frank Fiore, CPA — President & Visionary, Accounting Freedom

Frank Fiore has spent 20+ years helping small business owners in Illinois and Wisconsin stay compliant and represented when the IRS comes calling. Accounting Freedom serves clients from offices in Mundelein, IL and Grafton, WI.