How Illinois and Wisconsin Landscaping Companies Should Handle Cash Flow in the Off-Season

Every landscaping company in Illinois and Wisconsin faces the same landscaping cash flow reality: five or six months of strong revenue followed by several months of not much. The work stops. The expenses don’t.

Truck payments, insurance, equipment storage, administrative salaries, and your own draw — these costs run twelve months a year whether or not the crews are working. For landscaping companies that haven’t built a cash flow system around that reality, the off-season isn’t just slow. It’s stressful.

The good news is that landscaping cash flow problems are almost always predictable — and predictable problems can be planned for. This post covers the specific steps Illinois and Wisconsin landscaping companies should take to handle cash flow in the off-season: before it starts, during it, and coming out of it into spring.

The short version: Landscaping cash flow in the off-season comes down to four things: knowing your exact fixed cost exposure during slow months, building a cash reserve during peak season on purpose, structuring contracts and billing to smooth revenue across the year, and making the right tax and equipment decisions before December 31. Most landscaping companies handle the first two reactively. The ones that build real financial stability handle all four proactively — usually with an accounting firm that understands seasonal businesses.

Why Landscaping Cash Flow in Illinois and Wisconsin Is a Different Problem

Most cash flow advice for landscaping companies treats the off-season as a revenue problem: add snow removal, offer holiday lighting, stay busy. That’s reasonable operational advice. But it misses the accounting side of the equation — the decisions that determine whether a landscaping company survives and thrives financially, not just stays occupied.

Illinois and Wisconsin landscaping companies face a specific version of this challenge. The slow season in the upper Midwest typically runs November through March — four to five months. During that stretch, a landscaping company with $2M in peak-season revenue might collect $100,000 to $200,000 from snow removal contracts while carrying $40,000 to $60,000 per month in fixed overhead. The math requires intentional planning, not optimism.

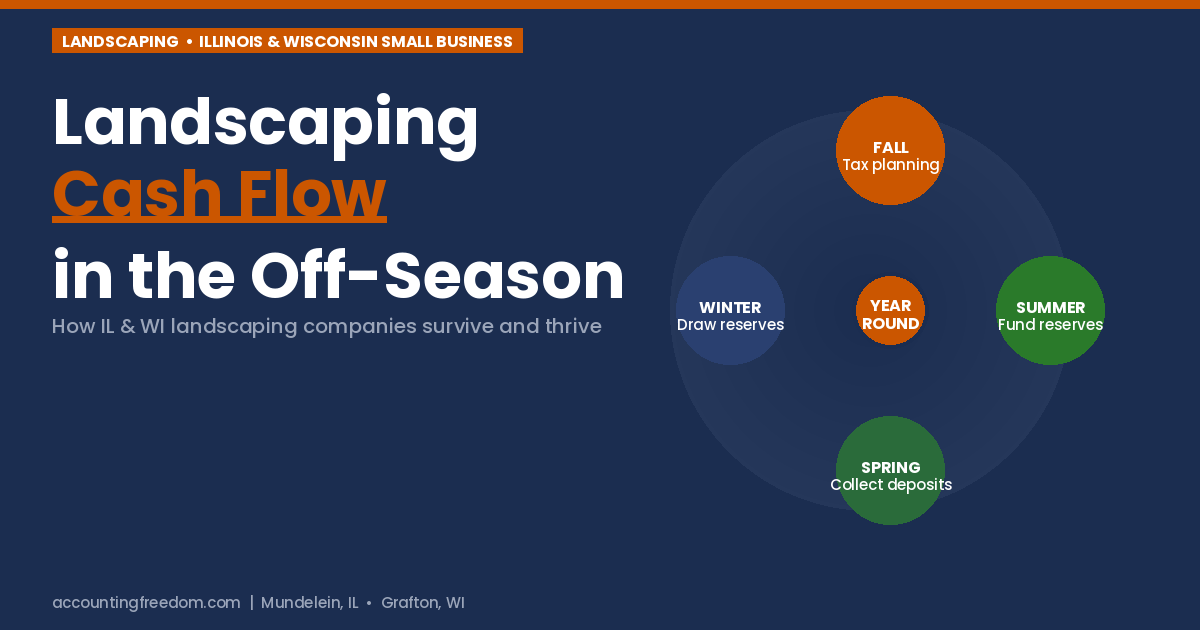

The Landscaping Cash Flow Calendar: What Should Be Happening Each Season

Landscaping cash flow management isn’t a one-time decision. It’s a series of actions tied to the calendar. Here’s what should be happening at each stage of the year for an Illinois or Wisconsin landscaping company running $1M–$3M in revenue.

| Season | Cash Flow Priority | Accounting Action |

|---|---|---|

| Spring (Mar–May) | Ramp up, collect deposits, lock in contracts | Review prior year P&L by service line; set reserve target for the year |

| Peak (Jun–Aug) | Maximize collections; fund reserve account | Monthly P&L review; automate reserve transfers; track job profitability |

| Pre-Winter (Sep–Oct) | Final equipment purchases; confirm snow contracts | Tax planning conversation — Section 179, retirement contributions, entity review |

| Off-Season (Nov–Mar) | Draw from reserves; manage fixed costs; collect snow billing | Monthly cash flow review; quarterly estimated tax payments; books current |

Calculate Your Off-Season Cash Requirement Before September

The most important number in landscaping cash flow management isn’t your peak-season revenue. It’s your fixed monthly overhead during the off-season multiplied by the number of slow months.

Start by listing every expense that runs whether or not you’re generating revenue: vehicle and equipment loan payments, insurance, storage facility costs, any year-round administrative or supervisory salaries, software, and your own draw. For most Illinois and Wisconsin landscaping companies in the $1M–$3M range, that number falls between $25,000 and $60,000 per month.

Multiply that by your expected slow season length — typically four to five months in this region. Then add a 25–30% buffer for unexpected equipment repairs, slow-paying snow customers, or a low-snowfall winter that reduces your snow revenue. That total is your target cash reserve balance entering November.

This calculation should happen every year in August or September — not in November when the window has closed. If your current accountant isn’t having this conversation with you before peak season ends, that’s a gap worth addressing. See our post on signs you’ve outgrown your accountant for what proactive advisory work actually looks like.

Build the Reserve Account During Peak Season — On Purpose

Knowing your reserve target is only useful if you actually fund it. The reason most landscaping companies enter winter underfunded isn’t ignorance — it’s that peak season cash feels abundant and the discipline to set it aside doesn’t happen automatically.

The fix is to automate it. Open a dedicated reserve account — separate from your operating account — and set up an automatic transfer every time a large payment clears. A simple rule: transfer 15–20% of every invoice over $5,000 directly to the reserve account the day it posts. During a $2M revenue season, that creates a $300,000–$400,000 reserve position before any deliberate decision-making is required.

Treat the reserve like a fixed overhead expense. It’s not discretionary. It’s not available for equipment upgrades, additional marketing spend, or owner distributions until the reserve target is met.

Structure Contracts and Billing to Smooth Landscaping Cash Flow Year-Round

Beyond reserves, the most effective way to manage landscaping cash flow is to reduce the severity of the seasonal swing through contract structure. Two approaches work well for Illinois and Wisconsin landscaping companies.

Annual Contracts Billed Monthly

Instead of billing for lawn maintenance by visit during the season, package annual maintenance into a flat monthly fee billed year-round. A client who pays $4,800 annually for lawn care gets billed $400/month, January through December. You collect $400 in January even though no mowing happens. Over a full client base, this structure meaningfully smooths winter cash flow and reduces the collection burden in spring when you’re already overwhelmed with ramp-up operations.

Deposits on Large Installation Projects

Landscape installation, hardscape, irrigation, and sod projects should never be fully financed by the contractor. A standard structure is 30–40% deposit at contract signing, 30–40% at project midpoint, and the balance at completion. For a $45,000 installation project, that means $13,500–$18,000 in your account before a crew member sets foot on the property. Deposits protect cash, reduce risk, and filter out customers who aren’t serious.

Make the Tax and Equipment Decisions Before December 31

For landscaping companies, the September–October window isn’t just the end of peak season. It’s the most important tax planning window of the year. The decisions made before December 31 determine the tax bill due the following April — and for profitable landscaping companies, that difference can be significant.

Section 179 and Bonus Depreciation

Landscaping companies carry significant equipment: mowers, trucks, trailers, plows, skid steers, irrigation systems. Under Section 179, qualifying equipment purchased and placed in service before December 31 can be fully deducted in the year of purchase rather than depreciated over time. For a landscaping company buying a $65,000 truck and a $28,000 mower in October, that’s a potential $93,000 deduction — but only if the purchase happens before year-end and is structured correctly.

This is the planning conversation that should happen in September, not February. If your accountant isn’t reaching out to you before October about equipment purchases and year-end tax moves, you’re likely leaving real money on the table every year.

Estimated Tax Payments and Cash Flow Timing

Quarterly estimated tax payments create an additional off-season cash flow challenge. The January 15 estimated payment — the fourth quarter installment — comes due right in the middle of the slow season. For a profitable landscaping company, that payment can be substantial. Planning for it in September means setting aside reserves specifically for the tax obligation, separate from the operating reserve. Failing to plan means the January payment either draws down operating cash at the worst possible time or creates an underpayment situation that carries penalties.

Retirement Plan Contributions

A SEP-IRA or Solo 401(k) contribution made before the tax deadline reduces taxable income directly. For a landscaping company owner with $180,000 in net profit, maximizing a SEP-IRA contribution can shelter $33,000–$45,000 from federal and state income tax. That’s a real number — and it’s only available if the plan exists and the decision is made before the filing deadline. For details on the right plan structure, see our guide to best retirement plans for small business owners.

Keep Books Current Through the Off-Season — Not Just at Tax Time

Off-season is when landscaping company books tend to fall behind. The urgency disappears, the volume slows down, and bookkeeping starts to feel less pressing. That’s exactly when staying current matters most.

Clean, current books through the winter give you an accurate picture of your reserve draw rate — how quickly you’re consuming the cash you built during peak season. Without current books, you’re making financial decisions based on a bank balance that doesn’t reflect outstanding obligations, and you lose the ability to course-correct before the situation becomes a problem.

Monthly financials through the off-season also give your advisor the data to have real conversations: Is the snow removal operation actually profitable, or is it subsidizing fixed overhead? Are you on track to enter spring with enough working capital for the ramp-up? These are questions your P&L can answer — but only if it’s current.

What This Means for Your Landscaping Business

The landscaping companies that handle the off-season well aren’t the ones with the most snow removal contracts or the most creative off-season services. They’re the ones that treated summer as a savings season, made their tax decisions in October, and entered November with a number — not a feeling — about whether they could make it to spring.

That level of financial visibility requires an accounting relationship, not just annual tax prep. At Accounting Freedom, we work with landscaping and snow removal businesses in Illinois and Wisconsin year-round — monthly books, proactive planning calls, and tax decisions made before year-end when they still matter.

- See what that looks like and what it costs: Use our pricing calculator — no email required.

- Read more about what we do for landscaping companies: Accounting for Landscaping & Snow Removal Companies

- Not sure which tier fits? Take our two-minute package assessment.

Want to know if your landscaping business is set up to handle the off-season?

That’s a 30-minute conversation. Free consultation, no pitch — just an honest look at your numbers and what we’d do differently.

Schedule a Free Consultation See Our PricingDisclaimer: This article is provided for general informational purposes only and does not constitute tax, legal, accounting, or financial advice. Every business situation is different. Before acting on anything you read here, please consult with a qualified advisor — including, we hope, us. Reach out to Accounting Freedom for guidance specific to your situation.

About the Author

Frank Fiore, CPA — President & Visionary, Accounting Freedom

Frank Fiore has spent 20+ years working with seasonal businesses, contractors, and landscaping companies across Illinois and Wisconsin. He’s seen firsthand what separates the companies that enter winter with confidence from the ones that enter it with stress — and it almost always comes down to the accounting decisions made before October 31. Accounting Freedom serves clients from offices in Mundelein, IL and Grafton, WI.